By Ulf Bergman

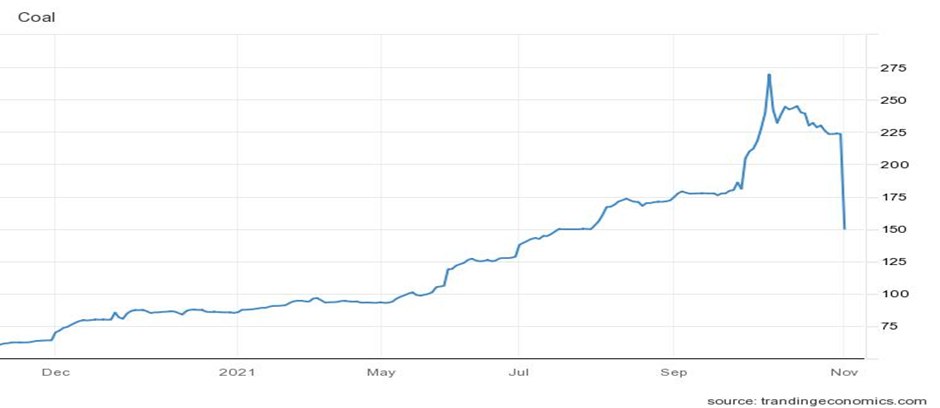

The new month has started rather dramatically for the coal markets. In the shadow of the United Nations’ COP26 summit on climate change, market prices for what is perceived to be one of the largest culprits are tumbling. The first trading session of the month saw gC Newcastle thermal coal futures dropping by a third to 150 dollars per tonne, which is the lowest since the end of July. In Europe, the price drop has been somewhat more modest. While parts of the continent saw markets closed on Monday due to All Saints’ Day, coal prices recorded a weekly decline of 24 per cent, bringing prices below 100 dollars per tonne for the first time since early August. Increasing output in Chinese mines has shifted the narrative, with markets turning increasingly bearish.

The much-published Chinese policy of coal “at all costs” appears to have given way to a greater focus on boosting domestic output. The country’s top economic planning agency, the National Development and Reform Commission, reported that the daily production from China’s coal mines has been above 11.5 million tonnes since the second half of October and about 1.1 million tons higher than at the end of the previous month. The NDRC has also previously stated that it is targeting a daily production of twelve million tonnes. At the same time, daily coal supply to the critical coal-fired power plants has reached 8.3 million tonnes, which is the highest ever recorded. The boost in domestic coal production has helped drive total coal inventories at Chinese power plants to 106 million tonnes, more than 28 million tonnes above what was recorded at the end of September. According to the NDRC, current stockpiles should support 19 days of consumption.

In parallel with the rising domestic output, seaborne imports have remained robust. According to data from Oceanbolt, 28.3 million tonnes of coal were discharged in Chinese ports during October. The volumes represented an increase of 120 per cent compared to the same month last year and were 2.2 million tonnes, or eight per cent, above the levels seen in September.

The improving supply situation is unlikely to signal the end of the energy crunch. Reports from US coal miners suggest that most of next year’s output has already been sold, with only minute export volumes remaining to be sold for delivery during the second half of next year. In Europe, natural gas supplies ahead of the winter remain uncertain after Russian exports through transit routes fell. Despite recent promises by the Russian President and Gazprom, supplies fail to match the European requirements. Hence, the lower coal prices are likely to be welcome news for many powerplants and further strengthen the current trend of coal substituting natural gas in the energy mix. In Germany, where coal-fired powerplants remain an essential part of energy production, power generation from solid fuel stations increased by nineteen per cent in October.

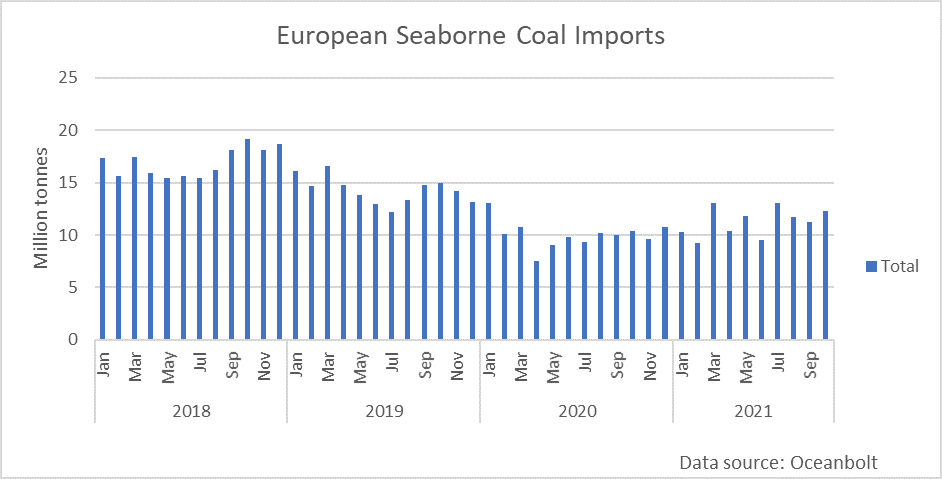

Perhaps somewhat ironic, European coal imports have rebounded during the build-up to the COP26 summit. The continent is often seen as a leading force in the decarbonisation campaign. However, after having declined for several years, monthly imports recovered during the early parts of the year, with last year’s total likely to be matched by the middle of November.

The current energy crisis highlights how dependent the world still is on coal as an energy source. While the increase in Chinese coal output has led to a considerable price fall in the last few days, prices remain very high in a historical context. Despite the epic drop, prices are still 150 per cent higher than a year ago. At this stage, it looks unlikely that global demand for the commodity will decrease materially any time soon and, with a lack of new coal mining projects, prices, therefore, look set to remain high. For dry bulk shipping, it will remain an important cargo. Global seaborne volumes have recovered from last year’s pandemic hit volumes but may not quite match the pre-pandemic peak recorded in 2019. However, second place is still a realistic possibility.