It is no secret that over the last two years Brazilian iron ore has been in short supply, mainly reflecting the major deadly dam incident in early 2019 as well as the COVID-19 pandemic this year which, combined with heavy rains in northern Brazil during the first half of the year, led to some of the lowest monthly exports out of the region in quite sometime. Yet, out of both of catastrophes, Brazil’s iron ore industry seems to be coming out in a better shape overall, as the back-to-back impacts of those events allowed major miners to push prices higher and better control their supply chains and, as a result, the ultimate selling price for their product and thus compensating for the lower volumes produced.

Indeed, there has been a scarcity of high quality iron ore in the world, and given the ever increasing Chinese demand for such product, mainly due to environmental issues but also steel mill profitability, headline iron ore prices (62%Fe) tend to move more dramatically during periods of short supply versus higher quality material (65%+Fe) which usually originates in Brazil. As the chart below shows, over the last two years, differentials for premium product (66% Fe in the chart) have shrunk, reflecting the mills’ appetite for any iron ore as the economies recovered and demand for steel increased.

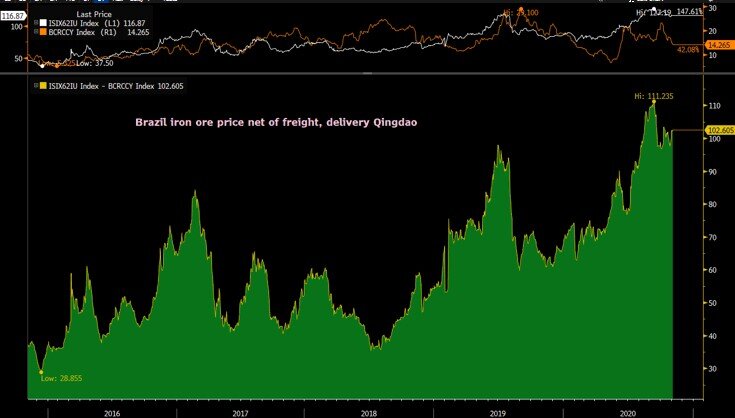

Yet, the above does not mean that Brazilian miners are actually suffering. To the contrary, their net-of-freight realized price is close to the highest level in many years, as headline prices have increased while freight costs have more or less remained staggered, as the chart below shows.

But is there really such a significant actual lack of high quality Brazilian product in the market or is that more of a result of a gradual artificial “price optimization” strategy out of the miners? At the end of the day, why premium differentials are not higher (see chart above) if indeed there is such a scarcity of product?

Vale, in their latest quarterly results provided some clues on their strategy of “optimizing” price over volume. For the third quarter, actual iron ore sales were some 11mt lower than actual production, the highest such spread in many years, as the chart below describes.

Indeed, Vale described their strategy of “rebuilding inventories” during the period in order to “optimize” their selling price for their product. After all, bringing their iron ore closer to the consumer (i.e. China) and managing their blending and logistics is to their advantage and better competes against the Australian miners who sit only 20 days away in terms of shipping lead times from China.

Such strategy has been in the works for the last few years, as the company aims at getting the best price available for their high quality iron ore, and their premium BRBF blend. And obviously, there is nothing wrong with that in a free market. However, BRBF is the most traded product in the spot market by a wide margin, as the table below shows, and with that comes the trading of spot freight to transport such spot cargoes, which makes the Brazil-China freight route the most important determinant of Capesize spot rates today.

On the inventory front, and with overall iron ore inventories in China at the highest level in 8 months, it is interesting to see what composition of such inventories. Unsurprisingly, the recent build up in onshore Chinese iron ore inventories reflect almost exclusively Brazilian iron ore and to a much lesser extend Australian:

Brazilian iron ore inventories in China

Australian iron ore inventories in China

Where does all the above leave the Capesize market’s near term outlook?

With Brazilian iron ore inventories back at the high end of their recent range in China, the “logistics optimization” strategy seem now more or less completed and as a result more spot cargoes of Brazilian iron ore should appear in the market. With that, more potential spot ships might be needed, which should be a welcomed development for Capesize owners.

The recent slow activity in Capesize rates might reflect Vale’s strategy of rebuilding inventories in China rather than selling directly to mills, which was done primarily in their own VLOC tonnage. As such strategy is now more or less completed, there is the potential of more direct sales of iron ore to end users and less shipping of material for inventory and blending. And with that a more active spot Capesize market might be in the works.